Business

Wealth Expert Reveals Four Strategies to Lower Inheritance Tax

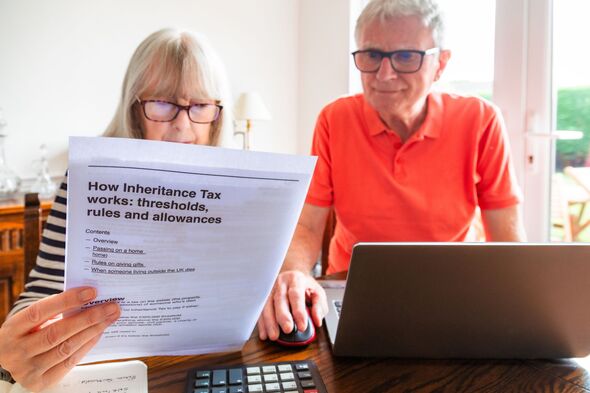

Inheritance tax (IHT) planning has become a pressing issue for many families in light of upcoming tax policy changes. Wealth managers have reported growing client concerns regarding potential liabilities as reforms to IHT rules come into effect. According to Simon Bashorun, head of advice at Rathbones Private Office, inquiries about estate planning have surged recently, particularly following the announcement that pensions will be included in taxable estates starting in 2027.

Bashorun cautioned families against making hasty decisions in response to these changes. “The freeze in IHT nil-rate bands has put families on a treadmill of rising inheritance tax liability,” he explained. This freeze, which affects both the main nil-rate band fixed at £325,000 since 2009 and the residence nil-rate band set at £175,000, is scheduled to remain in place until 2030. As a result, an increasing number of estates are becoming liable for IHT, leading to larger tax bills. Recent data revealed that nearly one in ten estates that paid IHT faced bills exceeding £500,000. If current trends continue, more than 3,500 estates could reach that threshold by 2026.

Bashorun emphasized the importance of a strategic approach to IHT planning. He stated, “Effective IHT planning starts with knowing what you can afford to give away.” This requires a comprehensive lifetime cash flow plan to evaluate one’s capacity to part with capital or income. Utilizing current allowances and reliefs is essential, and tailored financial advice is critical for establishing the best strategy according to individual circumstances.

While traditional strategies such as trusts and lifetime gifts remain popular, Bashorun highlighted four lesser-known methods that can help mitigate IHT liabilities.

Utilizing Deeds of Variation

One effective strategy is the use of a deed of variation, which allows beneficiaries to redirect an inheritance within two years of the death of the estate owner. This can enable the inheritance to pass to others, such as children or into a trust, which may reduce the estate’s IHT liability. Bashorun noted, “We are seeing rising interest in how a deed of variation can be used to redirect an expected inheritance. This not only provides protection from IHT but also greater control over the assets.”

Exploring Business Property Relief

Investors might also consider shares on the Alternative Investment Market (AIM), which can become exempt from IHT after two years through Business Property Relief (BPR). Although AIM shares have experienced a decline from their peak in 2021, Bashorun suggested that for clients with an appropriate risk appetite, AIM portfolios can still offer partial IHT savings. He warned, however, that the volatility associated with smaller company investments should not overshadow the investment’s fundamental value.

Certain unlisted companies and business assets may qualify for up to 100% IHT relief if held for at least two years and still owned at the time of death. Bashorun acknowledged the potential for shifts into other BPR investments and noted the uncertainty surrounding how transfers from AIM to BPR products will be treated. He advised a cautious ‘wait and see’ approach for those with the flexibility to do so.

Leveraging Regular Gifts from Surplus Income

Another strategy involves making regular gifts from surplus income, which can be immediately exempt from IHT as long as these gifts do not diminish the giver’s standard of living. “This exemption avoids the seven-year rule but remains underused,” Bashorun pointed out. Many individuals are simply unaware of this option.

As pensions are set to be included in taxable estates from 2027, families are reassessing their financial strategies. Bashorun highlighted that pension withdrawals can count as income, potentially triggering income tax. Paying 40% to 45% in taxes now may be preferable to facing a certain IHT charge later, especially for beneficiaries who are higher-rate taxpayers themselves.

Bashorun concluded by noting that families with significant surplus income are increasingly using it to fund discretionary trusts over time. This approach helps avoid large entry charges while transferring wealth into a structure that offers both protection and control for the family.

As families navigate the complexities of inheritance tax planning, understanding these lesser-known strategies could provide significant financial benefits and peace of mind. Seeking professional advice remains essential to tailor an effective plan that aligns with individual circumstances and goals.

Boxers from Bijelo Polje Prepare for Balkan Open Matches

DMGT Acquires Telegraph Media Group in £500 Million Deal

Junior Doctors Strike for Pay Increases as Pension Research Surfaces

Hull and East Yorkshire Business Awards Celebrate Local Achievements

Cardinal Onayekan Urges Nigerian Government to Act on Violence

US Lawmakers Criticize Andrew for Silence in Epstein Probe

Driving Instructor Reveals Quick Tips to Defog Windshields

Discover 4 Hidden Symptoms of Vitamin D Deficiency This Winter

Montenegro’s President Champions Budva as Tourism Driver

Neurologist Warns Excessive Use of Supplements Can Harm Brain

Fiona Phillips’ Husband Shares Heartfelt Update on Her Alzheimer’s Journey

Brian Cox Addresses Claims of Alien Probe in 3I/ATLAS Discovery

NASA Investigates Unusual Comet 3I/ATLAS; New Findings Emerge

Scientists Examine 3I/ATLAS: Alien Artifact or Cosmic Oddity?

Kerry Katona Discusses Future Baby Plans and Brian McFadden’s Wedding

NASA Investigates Speedy Object 3I/ATLAS, Sparking Speculation

Emmerdale Faces Tension as Dylan and April’s Lives Hang in the Balance

Cole Palmer’s Cryptic Message to Kobbie Mainoo Following Loan Talks

-

Health3 months ago

Health3 months agoNeurologist Warns Excessive Use of Supplements Can Harm Brain

-

Health3 months ago

Health3 months agoFiona Phillips’ Husband Shares Heartfelt Update on Her Alzheimer’s Journey

-

Science1 month ago

Science1 month agoBrian Cox Addresses Claims of Alien Probe in 3I/ATLAS Discovery

-

Science1 month ago

Science1 month agoNASA Investigates Unusual Comet 3I/ATLAS; New Findings Emerge

-

Science4 weeks ago

Science4 weeks agoScientists Examine 3I/ATLAS: Alien Artifact or Cosmic Oddity?

-

Entertainment4 months ago

Entertainment4 months agoKerry Katona Discusses Future Baby Plans and Brian McFadden’s Wedding

-

Science4 weeks ago

Science4 weeks agoNASA Investigates Speedy Object 3I/ATLAS, Sparking Speculation

-

Entertainment4 months ago

Entertainment4 months agoEmmerdale Faces Tension as Dylan and April’s Lives Hang in the Balance

-

World3 months ago

World3 months agoCole Palmer’s Cryptic Message to Kobbie Mainoo Following Loan Talks

-

Science4 weeks ago

Science4 weeks agoNASA Scientists Explore Origins of 3I/ATLAS, a Fast-Moving Visitor

-

Entertainment4 months ago

Entertainment4 months agoLove Island Star Toni Laite’s Mother Expresses Disappointment Over Coupling Decision

-

Entertainment3 months ago

Entertainment3 months agoMajor Cast Changes at Coronation Street: Exits and Returns in 2025